What you need to know about private pensions

Why should you make your own pension provision? We show you how easy it can be to save for retirement and how pillar 3a can help. When should you start, and how do you do manage everything easily?

Why should you make your own pension provision? We show you how easy it can be to save for retirement and how pillar 3a can help. When should you start, and how do you do manage everything easily?

For many of us, old age and retirement are some way off and the idea of a pension seems rather abstract – especially when we are still in the prime of our lives. We know that we’ll need it, but it’s not necessarily something we want to spend our time thinking about now. Retirement is simply too far in the future for that. If you feel the same way, you’re not alone.

But pension provision is like many things in life. Starting early and sticking at it will pay off in the long term, just like with fitness training, skiing, education or eating properly. That’s why it’s worth planning for your retirement now.

Ideally, you should start saving for retirement as soon as you enter into employment. It is possible to start at any time from the age of 18 onwards.

You can also still pay into the third pillar up to five years after you reach AHV retirement age. The only requirement is that you are gainfully employed in Switzerland and that you have an income subject to AHV contributions. To see the maximum amount you can pay in this year, click here.

Together, the AHV (pillar 1) and your pension fund (pillar 2) will probably only cover 60% to 70% of your income after you retire. The following points are also important to bear in mind:

To maintain your standard of living after you retire, you need a private pension.

> How does the pension system in Switzerland work?

Let’s assume you are 30 years old, female and have an annual income (gross) of CHF 60,000. If you retire at 64, you will receive an estimated CHF 37,200 (CHF 3,100 x 12 months) per year from the AHV and your pension fund, which is about 62% of your gross income of CHF 60,000.

In order to maintain your standard of living, you will need an additional CHF 14,400 each year.

Say you live to be 84 years old, that’s CHF 288,000. If you don’t have a private pension, you will most likely have to lower your standard of living. However, if you save privately, you can reduce or even avoid this gap.

Is it impossible to save CHF 288,000?

This sounds like a huge amount of money now, but is absolutely achievable.

Here’s how it might work:

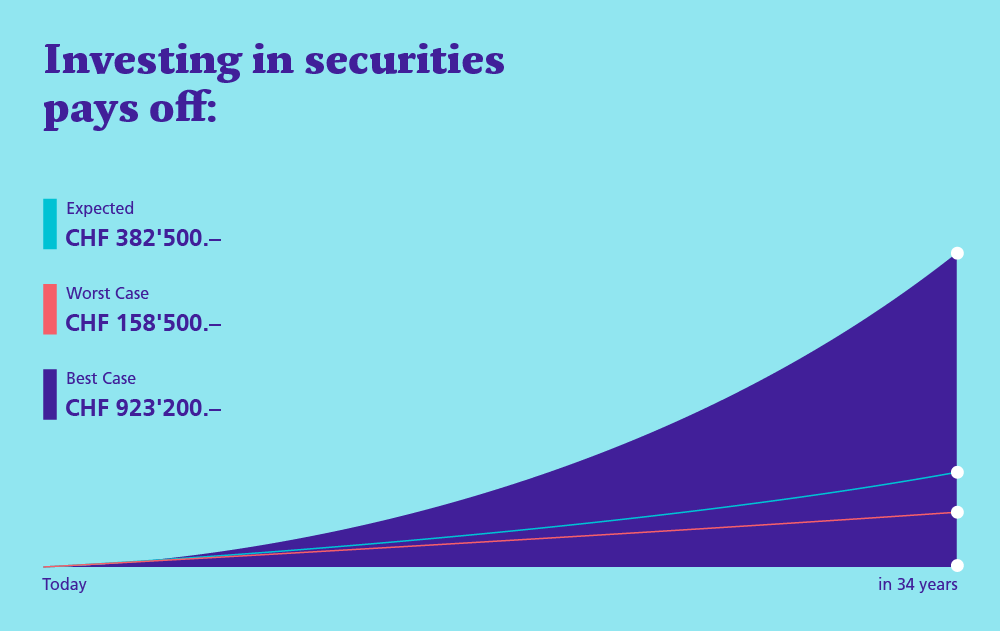

How does this work? By investing in securities and based on possible performance over time. You can run your own calculations using our pension calculator:

Assumption: Balanced investment strategy with a hypothetical return of 3.2% (net of costs). Securities savings may fluctuate, the hypothetical return cannot be guaranteed and tax effects are not included in this forecast.

Whether you feel more comfortable with securities or a savings account is a matter of preference. Unless you make an advance withdrawal for the reasons mentioned above, your retirement benefits will only be needed in the distant future and will often be paid in regularly (e.g. once a year). These are ideal conditions for exploiting the potential returns of securities.

The advantages and disadvantages of investing in securities:

Advantages:

Disadvantages:

Looked at from another perspective, when you invest in a savings account, your money feels safe but over time it can be imperceptibly eaten up by inflation. If you want to take less risk, you can opt for a combination of two different options. You can hold part of your pension assets in cash and the rest in securities.

CHF 100* voucher for the transfer of your pillar 3a to frankly >

Knowledge

© Sparen 3 pension foundation of Zürcher Kantonalbank

and Vested Benefits Foundation of Zürcher Kantonalbank

Please rotate device